Rosa Malgeri Manzo

E-MAIL: rmalgeri30@gmail.com;

Internationalization of food system: the case of canning industry

Corresponding Author

Affiliation

Rosa Malgeri Manzo 1

[1] Adviser, Research & Study Centre, Italy

Citation

Dr. Rosa Malgeri Manzo, Internationalization of food system: the case of canning industry(2016)SDRP Journal of Food Science & Technology 1(4)

Abstract

The food industry is the second largest manufacturing sector in Italy, not only for economic, but also for the role played in the social, environmental and cultural development of the country. Total employment offered by this sector is around 2.5 millions workers. These companies are mostly family-run, which often give rise to aggregations industrial highly competitive in the international arena thanks to factors such as originality, flexibility, speed and attention to detail. A particularly important role is played by the canning sector, which allows you to eat all year round vegetables collection only in a certain season. Italy is the third largest producer of tomatoes in the world and the collection of tomatoes destined for canning industrial takes place once a year, in the summer months. The \'La Doria SpA Group\' is the first Italian producer of peeled and chopped tomatoes and legumes preserved and the second largest producer of juices and fruit drinks.

This article aims to analyze the process of growth and internationalization of the food processing sector, analyzing the expansion of this company on the basis of data from field surveys, with attention to the role of Information and Communications Technology.

As we’ll see the \'La Doria Spa Group\', despite its size, has established itself successfully in the international context, thanks to export orientation, working relationships and acquiosition policy.

Introduction

In Italy the food industry plays a major role not only in the international competition, but also in terms of exports. In recent years the Italian agro-industrial system has created an increase in exports by 6.2% and imports increased by 5.2%. These results have a positive effect on the balance of (improvement of 13.3%), although the balance is still negative (-8.241 million euro). In particular, Italy made an export of food products amounted to 22.419 million euro, 6.9% of the total export value of the country.

The EU remains the leading trading partner in both exports and imports in the food system. Among the most important recipient countries of food sales there are Germany (4.59 million euro), France, the United States, followed by the UK and Spain. The Italian competitive advantage in terms of exports is supported by traditional products made in Italy.

We can identify three major food chains: the milk chain, the chain of sausages and canned pork and the chain of canned tomato paste.

The market for canned tomato is worth about 500 millions euro of which corresponds to a consumption of 393 million kg of product. It is a mature market showing a trend down slightly, especially in value, due in part to a reduction in the average price. The main segment is that of tomato sauce, which is worth 43% of the market value and 46% in volume, followed by the tomato pulp (29% in value and 25% in volume), the peeled (17% in value), from tomato concentrate (6%) and tomatoes (4%) (source: IRI I + S + Lsp at May 2011).

'La Doria', born in 1954 near Salerno (an Italian town in Campania region), is a Group leader in the production of tomato products, fruit juices and drinks of fruit and vegetables preserved. From the beginning, the great family commitment, experience in the field, the wealth of skills and competences acquired gradually, together with technological innovation, enable 'La Doria' to take on a role as an international leader in the canned food sector. Thanks to high volumes, the cost leadership, the wide range of production, excellent price/quality/service, the company has become the preferred supplier of chains such as Tesco, Sainsbury, Morrison, Asda/Wal-Mart, Lidl, Aldi, Ahold, Danske Supermarket, ICA abroad and Conad, Carrefour, Auchan and Selex in Italy.

The orientation of 'La Doria' towards products with higher added value and service, there is the ultimate goal of responding to changes in demand and to meet the new use functions required by today’s consumer [1-2].

In recent years the company’s activity has been characterized by several acquisitions, with the objective to strengthen its presence in the main areas and to increase the range of products offered [3-4].

After setting out the characteristics of the canning sector for the processing of tomatoes and the position of small Italian companies toward Information and Communications Technology (ICT), it will pass to the analysis of the process of growth and internationalization of the 'La Doria SpA Group', with the help of data from field surveys. In this way we will be offered a new contribution to the literature not very rich about internationalization of small businesses in the food processing sector.

Materials & Methods

Thanks to the canning sector can consume throughout the year harvest vegetables only in a certain season.

The increase of the quality of the treatments made it possible to minimize the loss of nutrients that might occur during processing.

The tomato harvesting can take place either manually or through the use of machinery, which subsequently select and distribute the product in packaging.

The processed tomato canning industry can be turned into various product categories, which differences depending on the techniques used and the characteristics of the finished product [5-6]. In general, there are four different types of processed tomatoes: whole peeled tomatoes - peeled - (preserved foods using fresh tomatoes whole, with the addition of tomato juice semiconcentrato and salt); peeled tomatoes in pieces - pulp - (preserves made with fresh tomatoes normally round variety, peeled and cut into pieces) [7-8]; the past (preserves prepared with fresh tomatoes, sieved and partially deprived of their water content); the concentrate (product obtained from tomato juice, which is concentrated to warm up to achieve different concentration levels).

At the industry level, moving from category to that of whole peeled concentrated, there is a process of increasing concentration, by cutting up and draining processes or cooking, with gradual removal of water [9-11]. Typically for the consumer a more concentrated processed tomato carries a lower cooking time, and then an increase of service value of the product itself, to the detriment, however, of the degree of freshness which decreases with the cooking processes and concentration.

In addition to traditional products are added tomato products. These products are added to the service, capable of improving the quality of life and time management of the consumer, as in the case of products ready for the microwave, sauces with elaborate recipes, sauces, ketchup and single-serve.

Italy is the third largest producer of tomatoes in the world. The first industries were born in the second half of the 800 slopes of Vesuvius with the production of the first canned peeled tomatoes, which were exported in particular in Great Britain and consumed by coal miners to combat silicosis. Subsequently, the peeled tomato concentrates were joined and, only in more recent times, the past and the tomato pulp [12-14].

The tomato industry is almost exclusively grown in the open field and the national area devoted to this crop is slightly over 75,000 acres, with a total production of 4 million and 793 thousand tons. The regions most affected by this production are Puglia and Emilia-Romagna, with respectively 37% and 33% of the total Italian production.

Italy, as well as being among the main world producers of industrial tomatoes, holds an important position in terms of export, with about 932,000 tons of processed tomatoes exported in the first six months of 2011. The 50% of the exported product Italy is made from tomatoes category, while past and pulp each represent only 14% of total exports [15-16]. It is important to note that while the figures for the domestic market taking into account only products intended for domestic consumption, data on the exportation of Italian processed tomatoes include all formats, including those for food service.

Italian consumption of processed tomatoes is about 35 kg per capita, and only just over 2 million tons of tomato (about 40%) are for the domestic market, while the rest of Italian production (60%) is intended both to exports to Europe (Germany, France, UK) that to other countries (including the US, Japan, Australia), with an export value of around 1.4 million euro [17-18].

In 2013 there was a reduction in production due to the summer drought, the suboptimal quality of the product and the limited availability of the same. Yet it has not been an increase in list prices since the sector has served the high inventory levels resulting from overproduction previous years.

However in the last few months of the year, the market for canned tomato was affected by the processing campaign of the summer months, characterized by a further decline in the quantity of fresh tomatoes past the transformation, equivalent to 4.1 million tons, down 12.8% compared with 4.7 million tons processed in 2012 and 19.6% compared to the average of the period 2008-2012, amounting to 5.1 million tons. In this context, characterized by supply reduction and the rising cost of raw materials, there has been an upward trend in selling prices of finished products.

The contraction of the Italian production of tomato in the past two years is due to several factors, such as the common goal of the various actors in the chain to avoid surpluses that damage both industries that farmers, purpose reached through a decline of land planted with tomatoes; the effects of the community reform dell’Ortofrutta (became fully operational in 2011) providing that grants to farmers regardless of the type of cultivation of plants and no longer, as happened previously, in function of the amount of cultivated tomato, led some farmers not efficient to move away from tomato cultivation which requires substantial investment [19-20]; acceleration of the process already underway for several years, to rationalize the sector, following the financial crisis that is affecting strongly the canneries small and uncompetitive [21-22]. The decline in domestic production, combined with the low level of stocks in the sector, represents a positive data for a more balanced market in terms of supply and demand and, consequently, for the prices of finished products influenced by the volumes on the market.

As regards ICT investments, ICT is one of the most important instruments to warrant a right flow of information through food supply chain. Yet in Italy there is a difficult relation between technologies and organizations. Italy spends too little in IT: 50% of PMI and 25% of large size companies are still unwilling to innovation, exploiting ICT technologies driver and proving thus not having understood that: more IT investments mean more productivity, more innovation, more ability to push the economy development or at least more capacity to react in case of crisis and difficulty at economic level, mainly due to the speed and accuracy with which information can be conveyed to the relevant actors. However even if on the one hand, there is the progressive demographic ageing and an inappropriate educational system for technological challenges that keeps more than half of the population far from the Internet services advantages. On the other hand, a considerable part of the population has been shown a strong interest in new technologies. Innovation and technology are two important factors for company growth, but a lot of small and medium enterprises still don’t perceive them as such. Strategy, market and organization are three main challenges successfully faced by only few Italian companies (especially in the North), because ICT are considered as costs rather than potentially profitable investments [23-24].

Results

'La Doria', a company listed on the MTA, STAR segment of the Italian Stock Exchange, is the leading Italian producer of vegetables and tomato products (pulp and peeled) and second of juices and fruit drinks. Following the recent acquisition of the Pa.fi.al. Group, 'La Doria' became the first Italian manufacturer of ready-made sauces private label and among the top European producers (ANSA).

The results at 31 March consolidate those achieved in the same period, the Pa.fi.al. Group acquired in November 2014, so the comparison with the first quarter of the previous year is not homogeneous.

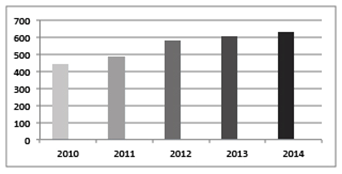

The total consolidated revenues amounted to € 185.5 million, up 19.5% from 155.3 millions in the first quarter of 2014, thanks mainly to the contribution of the line of sauces and growth lines legumes and vegetables and tomato products. They contributed to growth, both in international markets (+ 20.8%) that the domestic market (+ 14.4%).

The principal profit margins at consolidated level were: operating income, which amounted to 16.6 million from 12.1 millions in the first quarter 2014; EBIT, amounting to 13.3 million from 9.3 millions the 31.03.2014 (+ 43%, of which + 19.3% thanks to the contribution of Pa.fi.al.); profit before tax, which amounted to 12.6 million compared to 7.6 at 31 March 2014 (+ 65.8%, of which + 18.4% thanks to the acquisition); the Group’s net profit, which amounted to 7.3 million euro versus 3.8 millions in the first quarter 2014 (+ 92%, of which + 21% thanks to growth through acquisitions).

The portion attributable to minority interests amounted to 1.2 millions, the same amount over the same period last year.

The turnover of the parent company 'La Doria SpA' in the first quarter of 2015 is totalled 94.1 million, up 8.3% compared to 86.9 millions in the first quarter of 2014. The operating profit was 11.1 million, an increase of 24.7% compared with 8,6 of the first quarter 2014, while operating profit stood at 8.6 million, up 36.5% from the 6.3 million recorded as at 31 March 2014. The profit before tax amounted to 11.1 million, up 46% compared 7.6 million recorded the year before. The net result amounted to 8.3 million euro, an increase of 45.6% compared to 5,700,000 in the first quarter 2014.

The weakening of the euro in the first part of 2015 has helped sales, which would be up 13% at the same exchange rates. Net debt fell to 88.7 million euro, down from 138.2 million euro at 31 December 2014, while net assets amounted to 200 million.

In 2015 there was a strong increase in sales and profitability compared to the previous year, due both to organic growth and the acquisition of Pa.fi.al. Group.

La Doria has developed a good awareness of the strategic role of ICT. The company invests in ICT to meet the regulations on the traceability of food and especially to strengthen its orientation towards the effectiveness and efficiency of processes. The objective that we intend to achieve through the use of ICT is to work smarter and become more productive, but always within the traditional business. The ICT infrastructure presents a rather high degree of complexity. Most corporate functions find coverage of computer applications level. However some activities are carried out manually, even if supported by information systems.

Conclusion

The 'La Doria Spa Group', despite its size, has established itself successfully in the international context.

From the beginning, the company has a strong export orientation, with the search for emerging markets. It is also characterized by a structure oriented to marketing abroad, he has order established direct relationships with the trade and it is organized to manage the logistics of delivery and after-sales service in foreign countries. Among its strengths is particularly important orientation towards products with higher added value and service, strengthening of direct relationships with retailers and distributors English and the further growth of a strategic market like the UK.

The company has drawn its guidelines considering two important factors: the characteristics of the market for canned food plant, offering room for growth through innovation, segmentation and internationalization and the growth scenario for the tomato sector, due to a better balance between supply and demand.

The underlying objectives of the plan are to further increase the positions of 'La Doria Group' in the international market of tomato and vegetable-based private label and focus on the development of the domestic market of private labels. Equally priority is to improve the company’s profitability and further reducing debt.

The realization of these objectives took place through the implementation of strategies on which the company will focus its action in the next three years, such as: the further international expansion through the development of new markets, with a focus on emerging markets and the conquest of market share in the countries where the Group is currently under represented; the consolidation of leadership in the Italian market of juices in trademark and conquest, in that market, an important position also in tomato and legumes; the expansion of product lines and packaging of the most innovative and premium segments, more profitable; the growth of the market share of branded products on the Italian Cook UK market; continue to improve energy and industrial management.

Also the strategic process for the integration of technologies can lead the company to acquire a high degree of proficiency in respect of ICT potential. This does not mean that the company will actually be able to gain maximum benefit from these technologies, but there are the indispensable prerequisites so that ICT support the growth and improvement of the firm.

The 'La Doria' over the years has tried to institute the long-term relationships by developing products of partnership and working relationships that have allowed us to launch new products.

In addition, the acquisition of the Pa.fi.al. Group constitutes a significant strategic value for the 'La Doria Group' that aims to strengthen the leadership in the European market of private labels in its areas of reference.

Images and Tables